The Social Security Fairness Act, HR 82, (the “Act”) concerning the Windfall Elimination Provision and Government Pension Offset, was signed into law on January 5, 2025. Upon implementation, the Social Security Fairness Act eliminates the reduction of Social Security benefits while entitled to public pensions from work not covered by Social Security. The Social Security Administration is evaluating how to implement the Act.

The SSFA will restore and/or increase Social Security benefits for teachers, school cafeteria workers, custodians and other school employees, law enforcement officers, fire fighters, and other public servants by repealing two provisions of current law – the Windfall Elimination Provision (“WEP”) and the Government Pension Offset (“GPO”).

The Government Pension Offset states that If you receive a retirement or disability pension from a federal, state, or local government based on your own work for which you didn’t pay Social Security taxes, your Social Security benefits may be reduced (by two thirds of your pension payment). You may not receive any payment at all.

Example: If you get a monthly civil service pension of $3,000, two-thirds of that, or $2,000, must be deducted from your Social Security benefits. So, if you’re eligible for a $2,100 spouse’s or surviving spouse’s benefit from Social Security, you’ll get $100 a month ($2,100 – $2,000 = $100). If two-thirds of your government pension is more than your Social Security benefit, your benefit could be reduced to zero.

The Windfall Elimination Provision is a formula used to adjust Social Security worker benefits for people who receive “non-covered pensions” and qualify for Social Security benefits based on other Social Security–covered earnings. A non-covered pension is a pension paid by an employer that does not withhold Social Security taxes from your salary, typically, state and local governments or non-U.S. employers. Congress passed the WEP to prevent workers who receive non-covered pensions from receiving higher Social Security benefits as if they were long-time, low-wage earners.

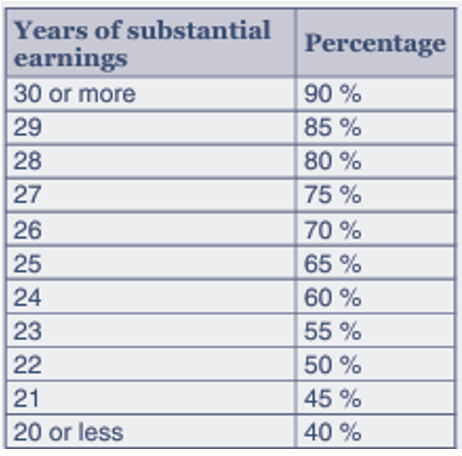

Example: When the WEP is applied, the percentage of career average earnings paid to lower-paid workers is greater than higher-paid workers. For example, consider workers age 62 in 2025, with average earnings of $3,000 per month. They could receive a benefit at FRA of $1,671 (approximately 55%) of their pre-retirement earnings increased by applicable cost of living adjustments (“COLAs”). For a worker with average earnings of $8,000 per month, the benefit starting at FRA could be $3,167.50 (approximately 39%) plus COLAs. The WEP was designed to adjust the percentage for the number of years of earnings where social security was paid (see table below thereby eliminating the ability of an individual to appear like a low wage earner and collect a higher percentage of pre-retirement earnings).

Source: Social Security Administration=

As the Act is effective December 31, 2023, the White House has stated that over two and a half million Americans are going to receive a lump-sum payment of thousands of dollars to make up for the shortfall in the benefits they should have gotten in 2024.

The White House has further stated that teachers, nurses, and other public and so- — employees and their spouses and survivors will receive an estimated average of $360 per month increase (if they paid into the Social Security system).

Bottom Line: Individuals who currently do not pay into the social security system, but have paid into the system in the past, can expect to receive higher benefits from social security upon retirement. The changes are estimated to be enough that they might warrant a change in the financial plans of affected individuals.