PDF Version: The Case for Tax-Free Municipal Bonds in a Richly Valued Equity Market

Executive Summary

U.S. equities are trading at some of the richest valuations in market history, while municipal bonds are offering after-tax income that competes with, or beats, equities on a risk-adjusted basis for taxable investors. We believe this combination argues for meaningfully increasing allocations to high-quality, tax-exempt municipal bonds — not as a defensive retreat from growth, but as a rational reallocation of portfolio risk at a point in the cycle when equity compensation for that risk has thinned.

Equities: Priced for Perfection

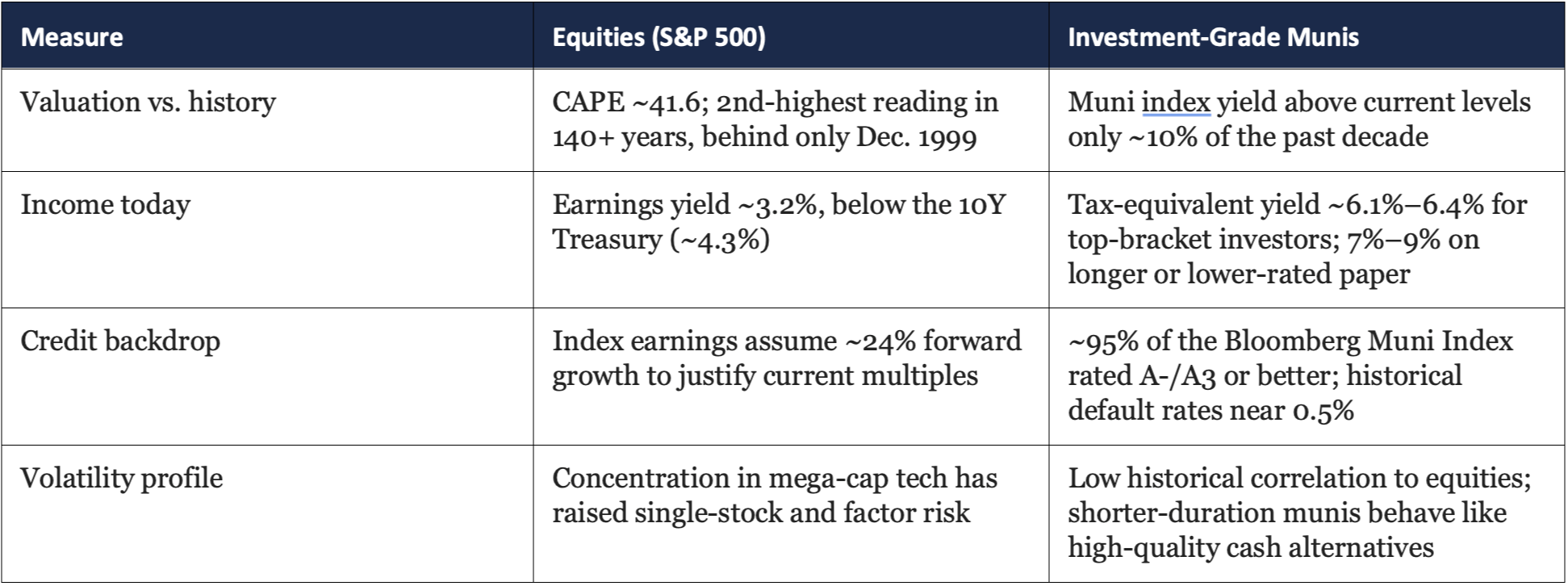

Multiple valuation lenses point the same direction. The Shiller CAPE ratio sits near 41.6 — more than double its long-run average of roughly 17.3, and the second-highest reading in over 140 years of data, trailing only the December 1999 peak. The traditional cyclically-adjusted P/E10 stands near 39.9, in roughly the 98th percentile of its historical range. On a trailing basis, the S&P 500 trades between the mid-20s and low-30s depending on methodology, comfortably above its 10- and 20-year medians.

Perhaps the more decision-useful signal for asset allocation is the earnings yield comparison: the S&P 500's earnings yield of roughly 3.2% now sits below the 10-year Treasury yield of about 4.3%. In other words, a risk-free government bond currently outyields the stock market's own earnings, before even considering the additional after-tax pickup available in municipals. Some strategists argue forward P/E multiples look more reasonable once expected earnings growth (aided by AI-related capital spending) is taken into account, and that accounting adjustments for stock-based compensation and intangibles bring the multiple down to a less extreme 22–23x. That debate is legitimate, and elevated valuations have historically persisted for extended periods without a correction. But even the more sanguine view concedes the market is "demanding," not cheap — and richly valued starting points have historically been associated with more muted 10-year forward real returns, even if the timing and magnitude of that mean reversion is highly uncertain.

Municipal Bonds: A Quietly Compelling Alternative

Attractive after-tax income

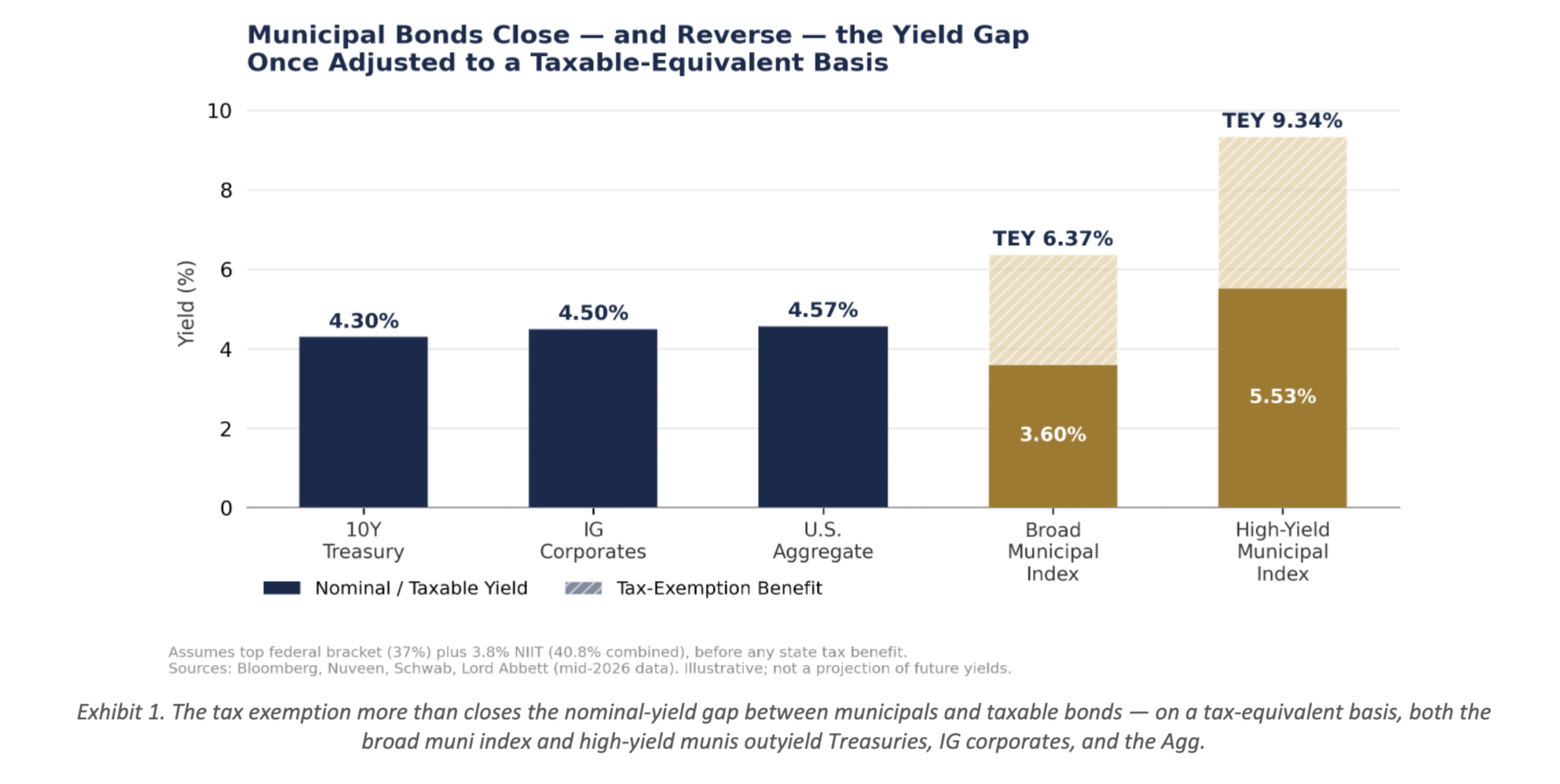

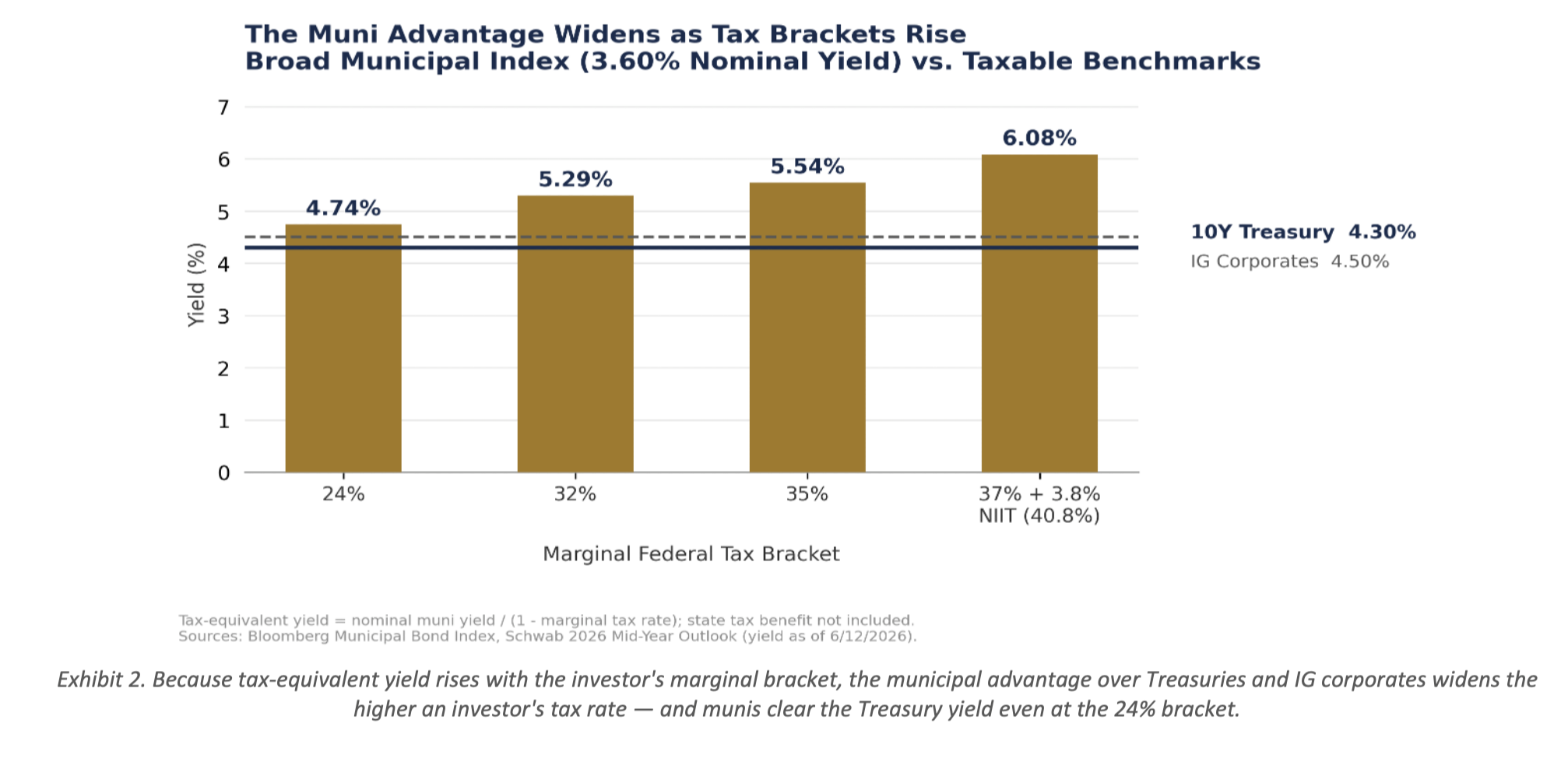

The broad Bloomberg Municipal Bond Index carried a yield to worst near 3.6% in mid-June 2026, translating to a taxable-equivalent yield of roughly 6% or more for a top-bracket investor before any state tax benefit. Nuveen puts the broad index's tax-equivalent yield at 6.37%, versus 4.57% for the taxable Bloomberg U.S. Aggregate — a meaningful spread. Investors willing to move down in credit quality or state tax reach higher still: the Bloomberg High Yield Municipal Bond Index yielded 5.53% as of late May, a 9.34% tax-equivalent yield at the top bracket. Longer-dated, higher-grade paper is attractive too — 20-year AA municipals currently offer a tax-equivalent yield near 7%, roughly 171 basis points above comparably rated 20-year AA corporates.

Strong credit fundamentals

Credit quality in the municipal market remains a genuine strength. Roughly 95% of the Bloomberg Municipal Bond Index is now rated A-/A3 or better, and historical default rates for investment-grade municipals remain near 0.5% — far below comparably rated corporate credit. State budgets have generally entered fiscal 2026 in solid shape, though rating agencies note growing dispersion among issuers and a modest uptick in downgrades relative to upgrades, a trend worth monitoring rather than ignoring.

Favorable technicals

Demand has been resilient even against a record pace of new issuance (roughly $600 billion projected for 2026). Municipal fund inflows reached roughly $50 billion in 2025 and have continued into 2026, and an estimated $8 trillion still sits in money market funds — a pool of capital that historically rotates back into bonds as the Federal Reserve eases and cash yields decline. The municipal yield curve is also unusually steep, with the 20-to-30-year spread near multi-year highs, rewarding investors willing to extend duration modestly for additional roll-down return.

The flow data through mid-2026 reinforces this picture. According to Lipper data cited by HilltopSecurities, municipal mutual funds have taken in nearly $25 billion year-to-date, with positive flows in 19 of the past 21 weeks and more than $1.5 billion in the most recent week alone. That demand trend traces back to May 2025 and accelerated through 2026 as investors prioritized stability, tax-exempt income, and increasingly attractive yields — a pattern consistent with money market balances leveling off and cash extending into longer-duration municipal exposure. HilltopSecurities also points to a widely discussed Wall Street Journal analysis suggesting equities' expected forward returns are running only modestly above what safe government bonds now offer, a dynamic likely reinforcing the rotation into munis.

Diversification value

Perhaps most relevant to the current equity backdrop, municipal bonds have historically shown low correlation to equity markets and lower volatility than corporate credit. In a portfolio context, high-quality munis can act as genuine ballast — ballast equities are currently not well positioned to provide for themselves, given depressed dividend and earnings yields relative to their own history.

Equities vs. Municipals: Side by Side

Risks and Balance

— Interest-rate risk: municipal bond prices, like all fixed income, fall when rates rise; longer-duration positioning increases this sensitivity.

— Elevated supply: near-record issuance could pressure yields higher (prices lower) if demand fails to keep pace, though technicals have absorbed supply well so far in 2026.

— Credit dispersion: downgrades have modestly outpaced upgrades in 2026; issuer selection matters more than broad-index exposure alone.

— Policy risk: municipal tax-exempt status faced legislative scrutiny in 2025 and was ultimately preserved. Budget reconciliation discussions have reportedly resurfaced in Washington in 2026, and while there is no defined legislative framework directly threatening the exemption at this stage, HilltopSecurities characterizes it as a developing signal worth monitoring rather than an imminent threat. The exemption remains a statutory privilege, not a guarantee.

— Equity valuations, while stretched, are not a market-timing signal — richly valued markets can remain richly valued, or become more so, for a long time. This note argues for rebalancing risk, not exiting equities.

Positioning Considerations for Burrows Capital Advisors Clients

For taxable investors in higher federal and state brackets, we see a reasonable case to lean into high-quality municipal bonds as a source of dependable, tax-efficient income while equity valuations digest an unusually rich starting point. A barbell approach — pairing short-dated municipals (five years and under) for liquidity and rate protection with selective exposure to the steep long end of the curve for additional yield and total-return potential — appears well suited to today's environment. Investors residing in no-income-tax states should weigh municipals against taxable alternatives more carefully, as the tax-exemption advantage is smaller for that group.

This note reflects general market conditions as of early July 2026 and is not a recommendation tailored to any individual's circumstances. Municipal bond suitability depends on an investor's tax bracket, state of residence, liquidity needs, and overall portfolio construction. We encourage clients to discuss specific allocation changes with their advisor at Burrows Capital Advisors and, where appropriate, a qualified tax professional.

Sources:

Bloomberg Municipal Bond Index and Bloomberg U.S. Aggregate Index data via Schwab, Nuveen, Lord Abbett, Morgan Stanley, AllianceBernstein, Breckinridge Capital Advisors, and Capital Group mid-year/2026 municipal outlooks (May–June 2026); municipal fund-flow and policy-risk commentary via Tom Kozlik, HilltopSecurities Municipal Commentary, "Investors are Choosing Stability, Tax-Exempt Income, and the Bonds that Finance America's Infrastructure" (May 2026, republished on AdvisorHub); S&P 500 valuation data via GuruFocus, multpl.com/Advisor Perspectives (Shiller CAPE and P/E10), StreetStats, VCP Scanner, and TradingView (May–July 2026).

This document is provided for informational purposes only and does not constitute investment, legal, or tax advice or an offer or solicitation to buy or sell any security. Bond investing involves risk, including loss of principal. Municipal bond income may be subject to state and local taxes and the alternative minimum tax. Past performance is not indicative of future results. Burrows Capital Advisors is not a licensed tax advisor; consult a qualified professional regarding your specific situation.

Asset allocation and diversification do not assure a profit or protect against loss in declining markets. Investors should consider their investment objectives, risk tolerance, time horizon, liquidity needs, and tax circumstances before implementing any portfolio allocation strategy.

Forward-looking statements are based upon current assumptions, expectations, and market conditions and are subject to change without notice. Actual results may differ materially from those anticipated. No assurance can be given that any forecasts or projections will be realized.